The Global Gold Rush

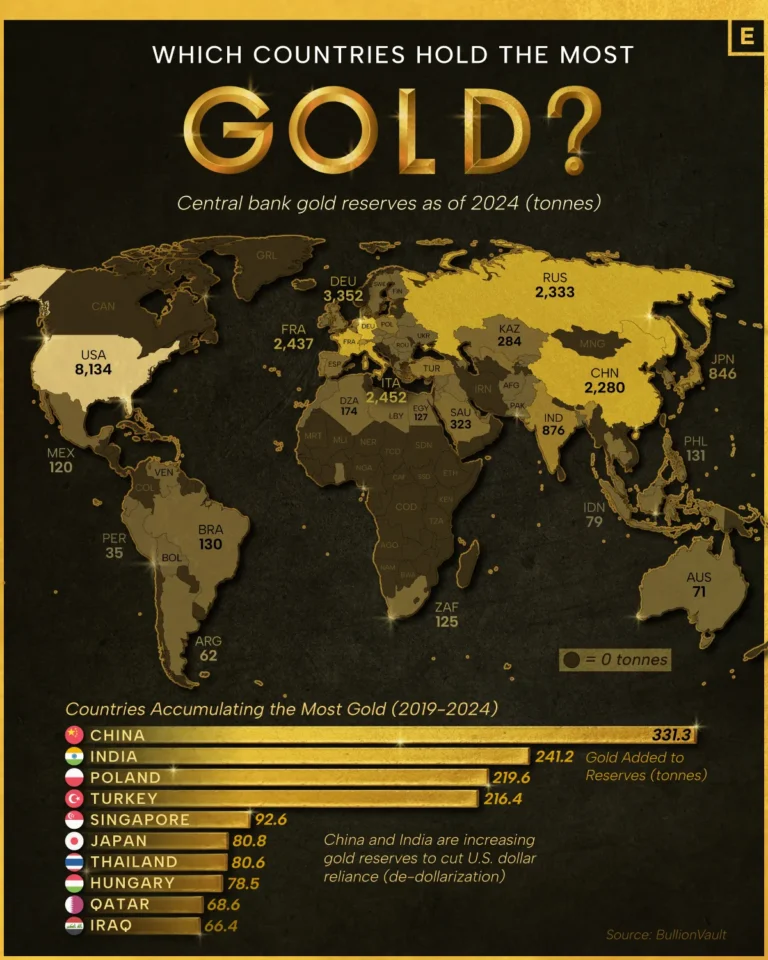

In this era of unprecedented economic uncertainty and shifting geopolitical alliances, the world’s central banks are engaged in a modern-day gold rush. According to recent data on central bank gold reserves, the United States maintains its position as the country with the largest gold holdings at 8,134 tonnes as of 2024. However, the more compelling story lies not in who holds the most gold, but in who’s been buying it most aggressively—and why this matters for the future of the global financial system.

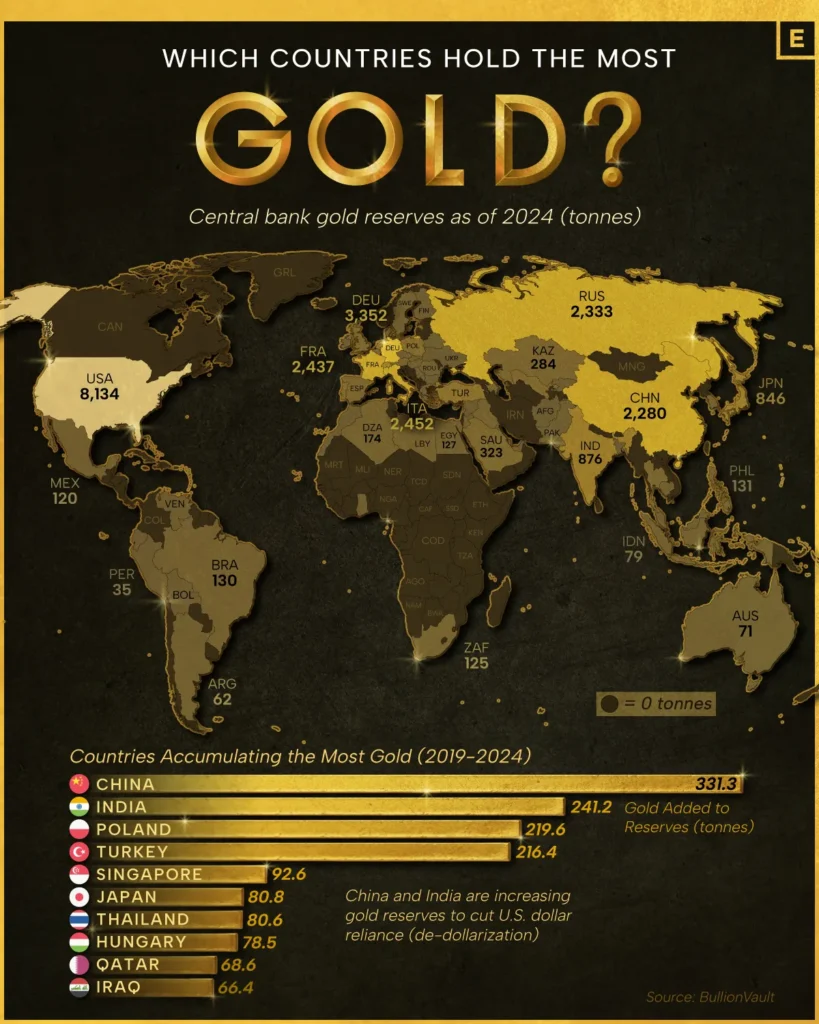

The Current Landscape of Gold Reserves

The United States’ gold reserves dwarf those of its closest competitors, representing a legacy of its post-World War II economic dominance and the Bretton Woods system. Germany follows with 3,352 tonnes, while Italy holds 2,452 tonnes. France maintains 2,437 tonnes, and Russia possesses 2,333 tonnes. China, the world’s second-largest economy, officially holds 2,280 tonnes, though many analysts believe the actual figure may be higher due to the opacity of Chinese reserve reporting.

Beyond the traditional powerhouses, other significant holders include India with 876 tonnes, Japan with 846 tonnes, and smaller but strategic buyers like Saudi Arabia with 323 tonnes and Kazakhstan with 284 tonnes. Even nations not typically associated with large reserves, such as Turkey and Poland, have emerged as notable players in the gold accumulation game.

China’s Aggressive Accumulation Strategy

The data reveals a striking trend: between 2019 and 2024, China led the world in gold accumulation, adding an impressive 331.3 tonnes to its reserves. This represents a deliberate, sustained campaign to diversify away from dollar-denominated assets and strengthen the yuan’s position in international trade. India follows closely behind with 241.2 tonnes added during the same period, while Poland accumulated 219.6 tonnes—a remarkable figure for a country of its size.

Turkey’s addition of 216.4 tonnes and Singapore’s 92.6 tonnes further illustrate that gold buying isn’t limited to traditional economic powers. Even smaller nations like Thailand (80.6 tonnes), Hungary (78.5 tonnes), Qatar (68.6 tonnes), and Iraq (66.4 tonnes) have joined the accumulation spree, suggesting a broader global shift in central bank strategy.

China’s six-year accumulation represents roughly a 17% increase in its gold reserves, signaling a strategic pivot in how the nation views its foreign exchange holdings. This isn’t merely about portfolio diversification—it’s about economic sovereignty and reducing vulnerability to Western sanctions and monetary policy decisions.

The De-Dollarization Agenda

The primary driver behind this gold-buying frenzy is the accelerating trend toward de-dollarization. For decades, the U.S. dollar has served as the world’s reserve currency, giving America enormous economic and geopolitical leverage. However, recent years have seen growing discomfort with this arrangement, particularly among nations that view dollar dominance as a strategic vulnerability.

The weaponization of the dollar through sanctions—particularly those imposed on Russia following its invasion of Ukraine—has sent shockwaves through the international financial system. Central banks worldwide watched as Russian reserves held in dollars were frozen, demonstrating that dollar assets aren’t truly sovereign when held by nations that might fall afoul of Western foreign policy. This realization has accelerated efforts to find alternatives.

Gold offers what dollars cannot: an asset that cannot be frozen, sanctioned, or devalued by another country’s monetary policy. Unlike digital currency reserves held in foreign banking systems, gold physically held within a nation’s borders is completely sovereign. For countries like China, Russia, and India—nations with aspirations of greater economic independence—gold represents financial insurance against geopolitical risk.

The rise of the BRICS nations (Brazil, Russia, India, China, and South Africa) and their discussions about creating alternative payment systems and potentially a gold-backed currency have further fueled this trend. While a BRICS currency remains largely theoretical, the conversations themselves indicate the seriousness with which these nations approach the challenge of dollar dependence.

Why Gold, Why Now?

Several factors have converged to make gold particularly attractive to central banks in recent years. First, persistent inflation in developed economies has eroded confidence in fiat currencies. When major central banks like the Federal Reserve and European Central Bank engage in massive monetary expansion—as they did during the COVID-19 pandemic—holders of those currencies inevitably seek stores of value that cannot be inflated away.

Second, geopolitical fragmentation has increased demand for neutral reserve assets. In a world of competing power blocs, gold serves as a universally accepted store of value that transcends political boundaries. Unlike the euro, yuan, or dollar, gold carries no counterparty risk and no political allegiance.

Third, historically low and even negative interest rates in many developed economies have reduced the opportunity cost of holding gold. When government bonds yield little to nothing, gold’s lack of yield becomes less of a disadvantage. As interest rates have risen more recently, gold has still maintained its appeal due to offsetting factors like inflation concerns and banking sector instability.

Fourth, the emergence of new gold trading mechanisms and the expansion of gold-backed financial products have made it easier for central banks to buy, store, and potentially mobilize gold reserves. The Shanghai Gold Exchange, for instance, provides an alternative to Western-dominated gold markets.

The Global Gold Supply Picture

Understanding the gold accumulation trend requires context about the global gold supply. Humanity has mined approximately 208,000 tonnes of gold throughout history, with roughly two-thirds of this mined since 1950. Of this total, central banks and international organizations hold about 35,000 tonnes—approximately 17% of all gold ever mined.

Current annual gold mine production stands at approximately 3,000 to 3,500 tonnes per year. This relatively modest supply growth—around 1.5% of existing above-ground stocks annually—is one reason gold maintains its value. Unlike fiat currency, which can be created with keystrokes, new gold supply is constrained by geology and the significant time and capital required to bring new mines into production.

China, Australia, Russia, and the United States lead global gold production, but even their combined output cannot satisfy global demand during periods of high central bank buying. This supply constraint means that sustained central bank accumulation can significantly impact gold prices and availability.

Additionally, gold recycling adds roughly 1,000 to 1,500 tonnes to the annual supply, primarily from jewelry and industrial applications. However, central banks are typically net buyers rather than sellers in the current environment, representing a structural change from earlier decades when Western central banks were often net sellers.

The Future of Gold in Central Bank Reserves

The trend toward gold accumulation shows no signs of slowing. As long as geopolitical tensions remain elevated, inflation concerns persist, and nations seek alternatives to dollar dependence, gold will maintain its appeal as a monetary anchor. The data from 2019 to 2024 likely represents the beginning of a longer-term shift rather than a temporary aberration.

For the global financial system, this has profound implications. A world where central banks hold larger gold reserves is one where the dollar’s monopoly on international reserves gradually erodes. This doesn’t necessarily mean the dollar will lose its reserve currency status, but it does suggest a more multipolar monetary system is emerging.

The yellow metal, prized by civilizations for millennia, has once again proven its enduring role as the ultimate form of money—one that requires no promise, bears no counterparty risk, and transcends the rise and fall of empires. In an uncertain world, that timeless quality has never been more valuable.